7 Reasons to List Your House This Holiday Season

Around this time each year, many homeowners decide to wait until after the holidays to list their houses. Similarly, others who already have their homes on the market remove their listings until the spring. Let’s unpack the top reasons why listing your house now or keeping it on the market this winter may be the best choice you can make.

Here are seven great reasons not to wait:

- Relocation buyers are out there now. Many companies are still hiring throughout the holidays, and they need their new employees to start as soon as possible.

- Purchasers who are looking for homes during the holidays are serious buyers and are ready to buy now.

- You can restrict the showings on your home to days and times that are most convenient for you. You will remain in control.

- Homes show better when decorated for the holidays.

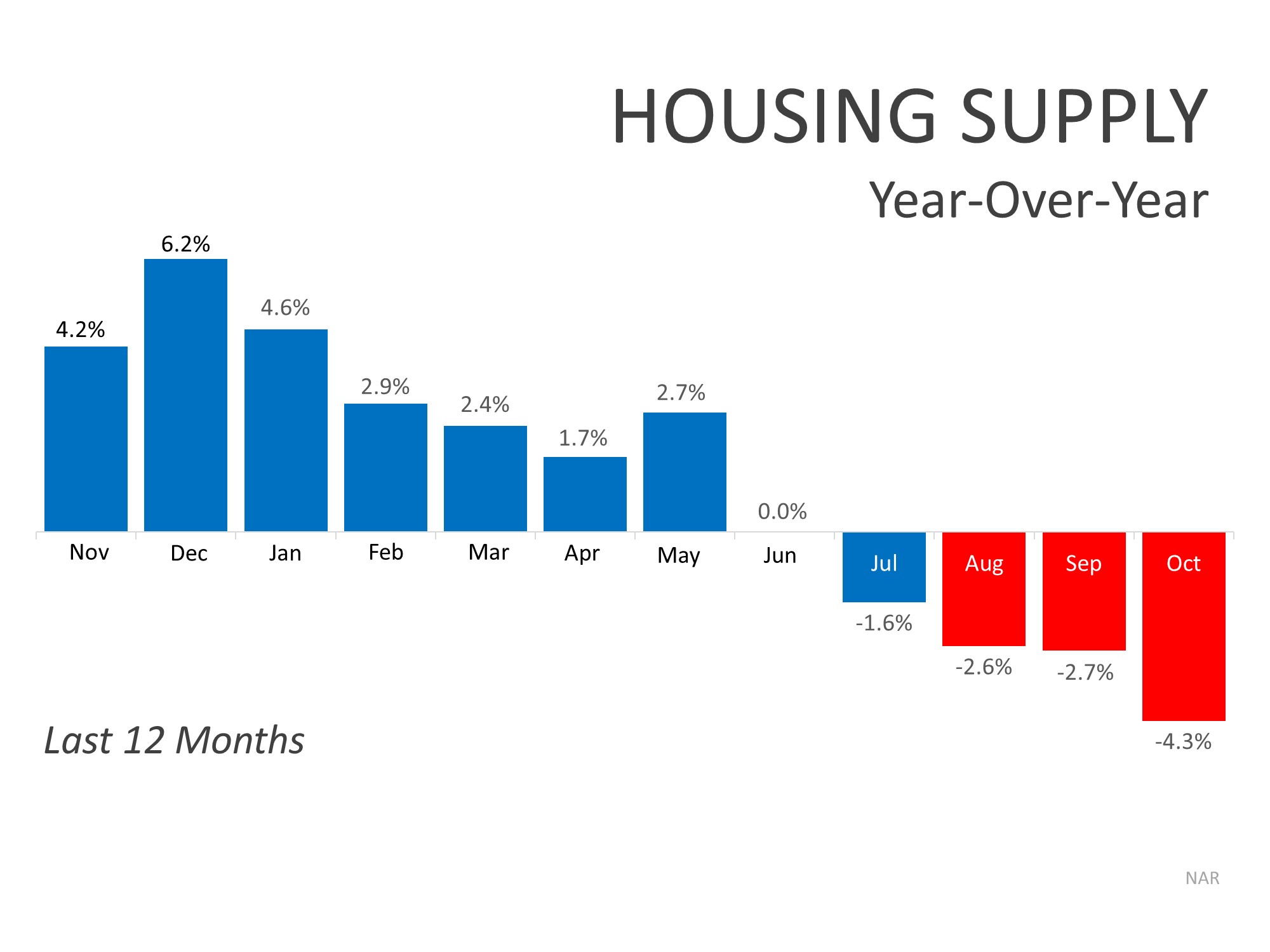

- There is minimal competition for you as a seller right now. Over the past few months we’ve seen the supply of homes for sale decreasing year-over-year, as shown in the graph below:

- The desire to own a home doesn’t stop during the holidays. Buyers who were unable to find their dream homes during the busy spring and summer months are still searching, and your home may be the answer.

- Late fall and early winter make up the “sweet spot” for sellers. The supply of listings increases substantially after the holidays. Also, in many parts of the country, new construction will continue to surge and reach new heights in 2020, which will lessen the demand for your house next year.

Bottom Line

It may make the most sense to list your home this holiday season. Let’s get together to determine if selling now is your best move.

![The Cost of Renting vs. Buying a Home [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2019/11/13082324/20191115-MEM-ENG.jpg)