Keys to Success for First-Time Homebuyers

Buying your first home is an exciting decision and a major milestone that has the power to change your life for the better. As a first-time homebuyer, it’s a vision you can bring to life, but, as the National Association of Realtors (NAR) shares, you’ll have to overcome some factors that have made it more challenging in recent years:

“Since 2011, the share of first-time home buyers has been under the historical norm of 40% as buyers face tight inventory, rising home prices, rising rents and high student debt loads.”

That said, if you’re looking to purchase your first home, here are two things you can consider to help make your dreams a reality.

Save Money with First-Time Homebuyer Programs

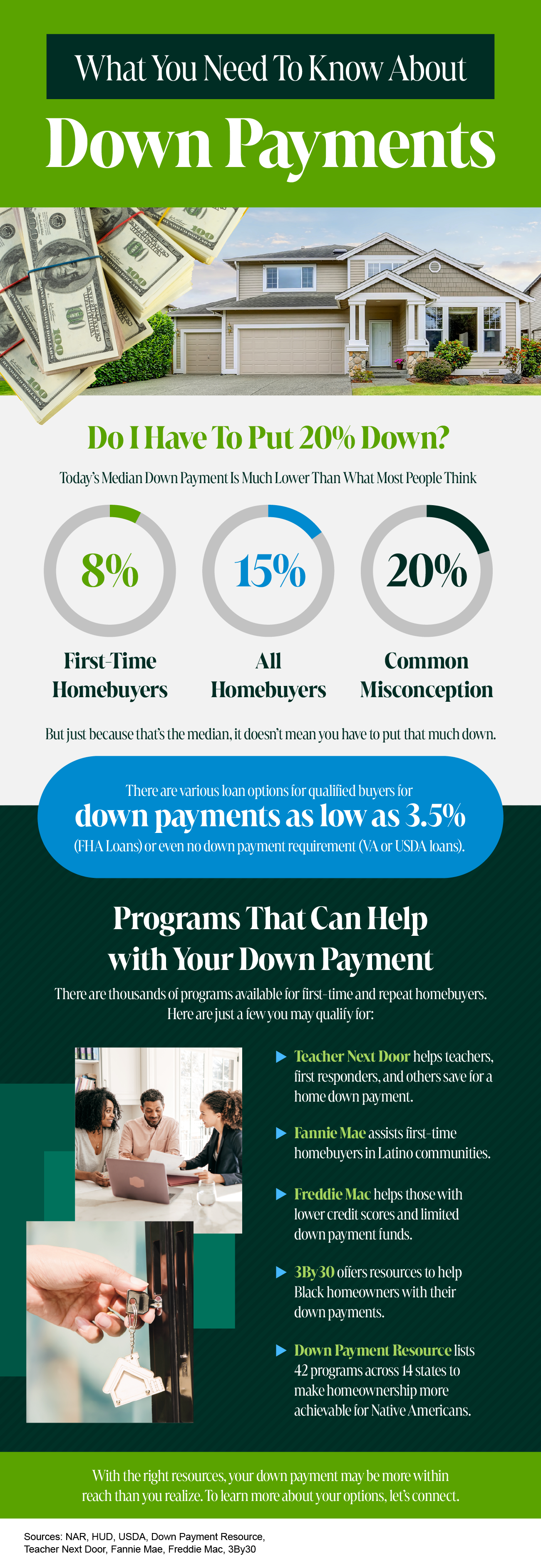

Being able to pay for the initial costs and fees associated with homeownership can feel like a major hurdle. Whether that’s getting a loan, being able to put together a down payment, or having money for closing costs – there are a variety of expenses that can make buying your first home feel challenging.

Fortunately, there are a lot of public and private first-time homebuyer programs that can help you get a loan with little-to-no money upfront. CNET explains:

“A first-time homebuyer program can help make homeownership more affordable and accessible by offering lower mortgage rates, down payment assistance and tax incentives.”

In fact, as Bankrate says, many of these programs are offered by state and local governments:

“Many states and local governments have programs that offer down payment or closing cost assistance – either low-interest-rate loans, deferred loans or even forgivable loans (aka grants) – to people looking to buy their first house . . .”

To take advantage of these programs, contact the housing authority in your state and browse sites like Down Payment Resource.

The Supply of Homes for Sale Is Low, So Explore Every Possibility

It’s a sellers’ market, meaning there aren’t enough homes on the market to meet buyer demand. So, how can you be sure you’re doing everything you can to find a home that works for you? You can increase your options by considering condominiums (condos) and townhomes. U.S. News tells us these housing types are often less expensive than single-family homes:

“Condos are usually less expensive than standalone houses . . . They are also less expensive to insure.”

One reason why they may be more affordable is because they’re often smaller. But they still give you the chance to get your foot in the door and achieve your dream of owning and building equity. Beyond that, another major perk is they typically require less maintenance. As U.S. News says in the same article:

“The strongest reason for purchasing a condo is that all external maintenance is usually covered by the condo association, such as landscaping, pool maintenance, external painting, paving, plowing and more. This fee also covers some internal maintenance, such as gas, electric, plumbing, HVAC and other mechanical systems.”

Townhomes and condos are great ways to get into homeownership. Owning your home allows you to build equity, increase your net worth, and can fuel a future move.

The best way to make sure you’re set up for success, especially if you’re just starting out, is to work with a trusted real estate agent. They can educate you on the homebuying process, help you understand your local area to find options that are right for you, and coach you through making an offer in a competitive market.

Bottom Line

Today’s housing market provides some challenges for first-time homebuyers. But, there are still ways to achieve your goals, like utilizing first-time homebuyer programs and considering all of your housing options. Let’s connect so you have an expert on your side who can help you navigate the process.

![You May Not Need as Much as You Think for Your Down Payment [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2023/02/01164441/You-May-Not-Need-As-Much-As-You-Think-For-Your-Down-Payment-MEM-1046x1917.png)

![Key Terms To Know When Buying a Home [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2023/01/11164544/Key-Terms-To-Know-When-Buying-A-Home-MEM-1046x2684.png)

![VA Loans: Making Homes for the Brave Achievable [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/11/09154718/VA-Loans-Making-Homes-For-The-Brave-Achievable-MEM-1046x2014.png)