Is Your House “Priced to Sell Immediately”?

In today’s real estate market, more houses are coming to market every day. Eager buyers are searching for their dream homes, so setting the right price for your house is one of the most important things you can do.

According to CoreLogic’s latest Home Price Index, home values have risen at over 6% a year over the past two years, but have started to slow to 3.6% over the last 12 months. By this time next year, CoreLogic predicts home values will be 5.4% higher.

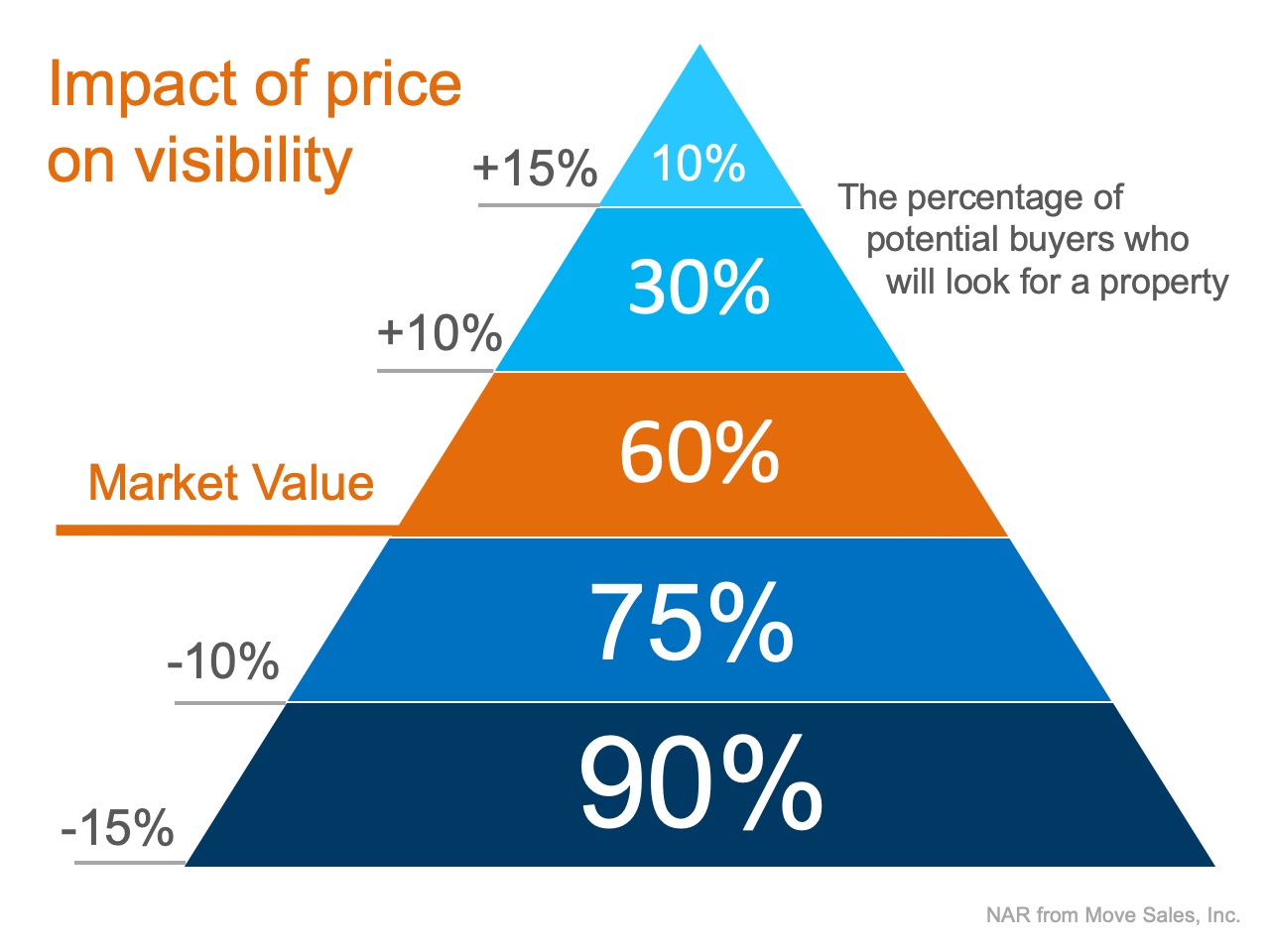

With prices slowing from their previous pace, homeowners must realize that pricing their homes a little over market value to leave room for negotiation will actually dramatically decrease the number of buyers who will see their listing (see the chart below). Instead of the seller trying to ‘win’ the negotiation with one buyer, they should price their house so demand for the home is maximized. By doing so, the seller will not be negotiating with a buyer over the price, but will instead have multiple buyers competing with each other over the house.

Instead of the seller trying to ‘win’ the negotiation with one buyer, they should price their house so demand for the home is maximized. By doing so, the seller will not be negotiating with a buyer over the price, but will instead have multiple buyers competing with each other over the house.

Instead of the seller trying to ‘win’ the negotiation with one buyer, they should price their house so demand for the home is maximized. By doing so, the seller will not be negotiating with a buyer over the price, but will instead have multiple buyers competing with each other over the house.

Instead of the seller trying to ‘win’ the negotiation with one buyer, they should price their house so demand for the home is maximized. By doing so, the seller will not be negotiating with a buyer over the price, but will instead have multiple buyers competing with each other over the house.

The secret is making sure your house is Priced To Sell Immediately (PTSI). That way, your home will be seen by the most potential buyers. It will sell at a great price before more competition comes to the market.

Bottom Line

If you're debating listing your house for sale, let’s get together to discuss how to price your home appropriately and maximize your exposure.

![4 Reasons to Sell This Fall [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2019/09/19104136/20190920-MEM-1046x808.jpg)