Homeowners Today Have Options To Avoid Foreclosure

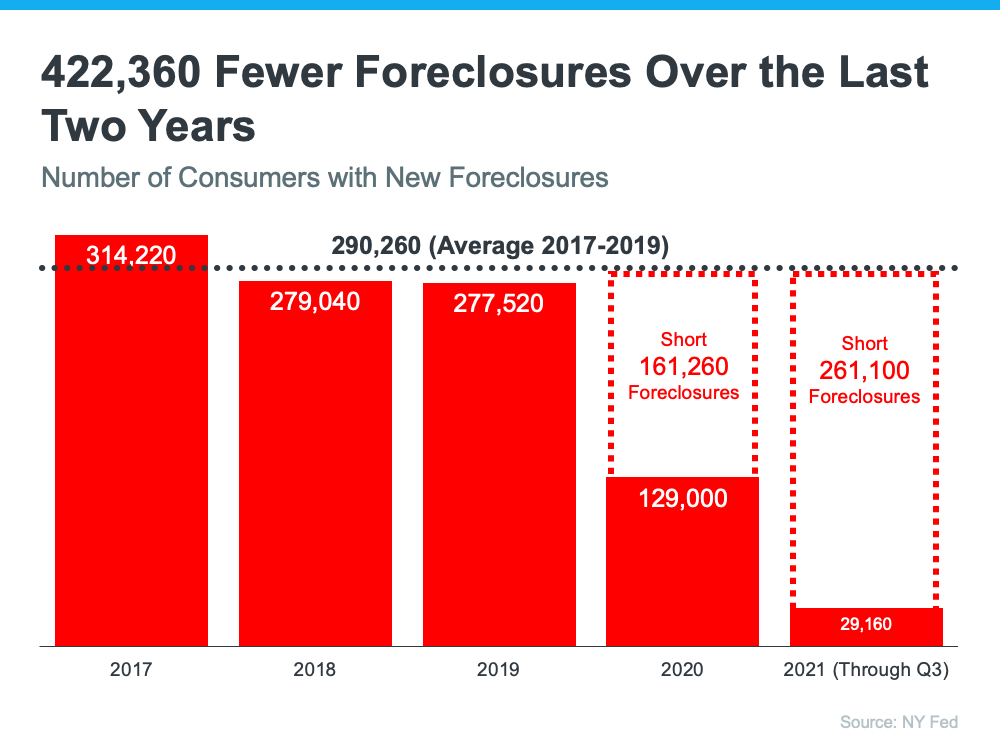

Even with the latest data coming in, the experts agree there’s no chance of a large-scale foreclosure crisis like the one we saw back in 2008. While headlines may be calling attention to a slight uptick in foreclosure filings recently, the bigger picture is that we’re still well below the number we’d see in a more normal year for the housing market. As a report from BlackKnight explains:

“The prospect of any kind of near-term surge in foreclosure activity remains low, with start volumes still nearly 40% below pre-pandemic levels.”

That’s good news. It means the number of homeowners at risk is very low compared to the norm.

But, there’s a small percentage who may be coming face to face with foreclosure as a possibility. That’s because some homeowners may have an unexpected hardship in their life, which unfortunately can happen in any market.

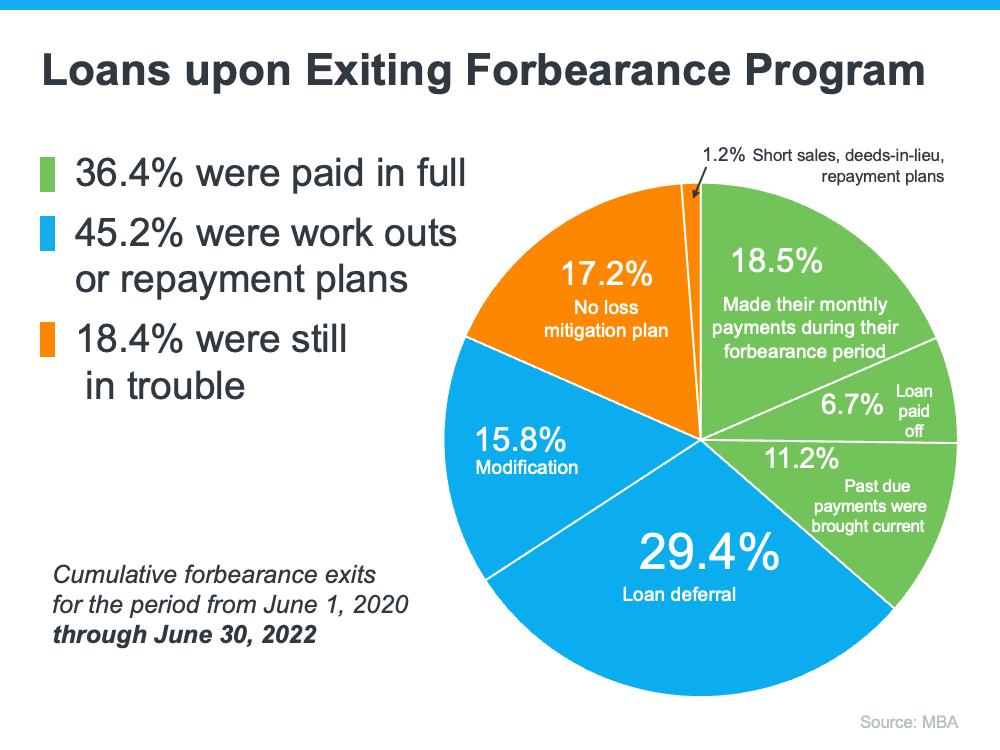

For those homeowners, there are still options that could help them avoid having to go through the foreclosure process. If you’re facing difficulties yourself, an article from Bankrate breaks down some things to explore:

- Look into Forbearance Programs: If you have a loan from Fannie Mae or Freddie Mac, you may be able to apply for this type of program.

- Ask for a loan modification: Your lender may be willing to adjust your loan terms to help bring down your monthly payment to something more achievable.

- Get a repayment plan in place: A lender may be able to set up a deferral or a payment plan if you’re not in a place where you’re able to make your payment.

And there’s something else you may want to consider. That’s whether you have enough equity in your home to sell it and protect your investment.

You May Be Able To Use Your Equity To Sell Your House

In today’s real estate market, many homeowners have far more equity in their homes than they realize due to the rapid home price appreciation we’ve seen over the past few years. That means, if you’ve lived in your house for a while, chances are your home’s value has gone up. Plus, the mortgage payments you’ve made during that time have chipped away at the balance of your loan. That combo may have given your equity a boost. And if your home’s current value is higher than what you still owe on your loan, you may be able to use that increase to your advantage. Freddie Mac explains how this can help:

“If you have enough equity, you can use the proceeds from the sale of your home to pay off your remaining mortgage debt, including any missed mortgage payments or other debts secured by your home.”

Lean on Experts To Explore Your Options

To find out how much equity you have, partner with a local real estate agent. They can give you an estimate of what your house could sell for based on recent sales of similar homes in your area. You may be able to sell your house to avoid foreclosure.

Bottom Line

If you’re a homeowner facing hardship, lean on a real estate professional to explore your options or see if you can sell your house to avoid foreclosure.